The 2023 market rally caught many people by surprise: most economists were expecting tepid growth or even a contraction in markets. But when you scratch the surface, it’s clear that most of the growth, in US markets in particular, was due to an AI-driven rally in mega-cap technology stocks. The breadth of the rally was fairly narrow and there was a large disparity in returns between the top performers and the rest of the market. Given the recent outperformance by the ‘Magnificent Seven’ and other AI-related technology stocks, and the popular US indices significantly overweight technology, many investors are looking to diversify to reduce risk.

After lagging their large cap peers over the last 3 years, one area which is generating significant interest right now is small and mid cap stocks. This article looks at whether now could be the right time to allocate to smaller companies, with a particular focus on global small and mid-caps (SMIDs).

Global SMID caps have underperformed and valuations are attractive

Historically, global SMID caps have delivered stronger returns than global large caps. Global SMID caps have outperformed global large caps for 61% of the time for 3-year rolling returns*.

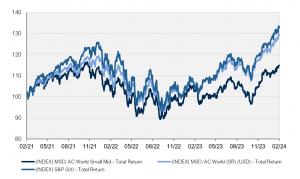

But whereas the long-term numbers favour SMID caps, the situation has been reversed in recent years. Global SMIDs have lagged large caps over the last 3 years as the chart below shows.

Source: Factset, total return, February 2021 to February 2024. Past performance is not a reliable indicator of future performance.

This valuation performance gap has become more pronounced over the past year as the large cap indices, buoyed by the mega-cap tech stocks, surged further ahead of global SMIDs.

Global SMIDs now look very attractive on both an absolute basis, and relative to historical measures. In addition, as you can see in the graph below, the premium valuation that Global SMIDs have historically shown vs large caps is no longer present.

Source: Factset, trailing 12 Month Price to Free Cash Flow, Feb 2014 to Feb 2024. Past performance is not a reliable indicator of future performance.

We are likely to see a rotation to smaller stocks this year

As any long-term investor knows, trying to finely time the market is an excellent way to set yourself up for stress and disappointment. However, over the longer-term, markets tend to revert to norms and follow similar cycles and historical patterns. There are several factors which have been impeding the growth of smaller companies and these are likely to turn throughout the year.

Smaller companies are more sensitive to interest rates; tending to struggle in a higher interest rate environment. They also generally find it harder to issue bonds and pay more for credit than larger companies. This trend is increased when markets are volatile: credit spreads tend to widen, increasing the gap between what the smallest and largest companies pay for credit, and putting smaller companies at a competitive disadvantage.

According to James Eisenman, portfolio manager Vaughan Nelson Equity SMID Fund the economic cycle may also benefit smaller companies this year:

“Smaller companies tend to move more cyclically than larger companies. With global growth set to bottom over the next two quarters and an acceleration in growth likely in the back half of 2024, the setup is attractive for Global SMIDs”

All smaller companies will not rise in unison

While conditions, in general, look favourable for smaller companies over the medium to long term, this does not mean all smaller companies will rise equally. When you reach the lower end of small cap indices there is a much higher proportion of unprofitable and speculative companies. For example there are many more speculative and unprofitable companies in an index like the Russell 2000, than in the MSCI ACWI SMID Cap Index, as it has much larger, more established companies. Now that interest rates are higher and capital has a real cost once more, many of these unprofitable companies have been burning through their funds. While corporate bankruptcy rates in the US rose significantly in 2023 they are still far lower than they were a decade ago. There remain many publicly listed companies struggling to survive and many of these are likely to go under this year.

In any market cycle there are always investment opportunities, the difficulty is in identifying them. For example, last year regional banks in the US had a torrid time. After Silicon Valley Bank became troubled, all US regional banks were sold off, no matter what their underlying fundamentals were like. The US Regional Banking Index was down 44% from February 7, 2023 to its low on May 4, 2023. For James Eisenman, this created an opportunity to pick up high-quality banking names at bargain prices.

“We started investing in two U.S. regional banks in the back half of 2023. It was clear to us that these banks had strong fundamentals and they had been sold off indiscriminately by investors. These banks rose significantly during the Q4 2023 equity rally, making us an excellent profit. While this is obviously an ideal investing scenario, we would have been happy to wait much longer than this for our profits as we were confident that we had bought quality companies that were undervalued by the market.”

In the same way as regional banks, there is an opportunity, right now, to buy companies in the global SMID space that can benefit from the same AI themes that have driven Nvidia and other big tech companies to eye-popping valuations. However, unlike Nvidia, they are much less known by investors, covered less by analysts, and so have much lower valuations. Unfortunately, like any red-hot investing theme, there are many companies trying to catch a ride on the AI-train. Many investing presentations and company reports are peppered with AI-buzzwords and it takes detailed bottom up fundamental stock analysis to separate real value from the value traps – true growth stocks from meme stocks.

When will small cap stocks rally?

Trying to time market rallies is like catching a baseball between your teeth: you may end up looking like a hero, but you’re much more likely to end up with a black eye. While conditions seem favourable for small and mid-cap companies this year, working out exactly when they will rally is almost impossible. We do know that when interest rates drop, this is likely to be beneficial for all stocks, but particularly smaller companies. In addition, we are in a US election year and both the US Federal Reserve and the US Federal Government have a vested interest in boosting the economy closer to election time which is also likely to provide strong support to markets.

Valuations for global SMID caps look attractive on an absolute basis and relative to history. While we wouldn’t recommend blindly investing in a swathe of smaller caps, we do think that the first half of this year is likely to be a good time to increase your allocation to high-quality small and medium-sized companies.

Australian investors can access Vaughan Nelson’s best investment ideas in global small-mid (SMID) cap expertise as a managed fund Global Equity SMID Fund and an active ETF ASX:VNGS Global Equity SMID Fund (Quoted Managed Fund)

*Source: Morningstar Direct. Comparing rolling 3-year returns (stepping forward in monthly increments) from the MSCI AC World Index and the MSCI AC World SMID Index for the period January 1, 2004 to December 31, 2023. Returns are net of fees and expressed in AUD. Past performance is not a reliable indicator of future performance.

This publication (the material) has been prepared and distributed by Natixis Investment Managers Australia Pty Limited AFSL 246830 and includes information provided by third parties, including Investors Mutual Limited (“IML”) AFSL 229988.

Although Natixis Investment Managers Australia Pty Limited believes that the material is correct, no warranty of accuracy, reliability or completeness is given, including for information provided by third parties, except for liability under statute which cannot be excluded. The material is for general information only and does not take into account your personal objectives, financial situation or needs. You should consider, and consult with your professional adviser, whether the information is suitable for your circumstances. Before deciding to acquire or continue to hold an investment in the Fund, you should consider the information contained in the Product Disclosure Statement in conjunction with the Target Market Determination, available free of charge from us.

Past investment performance is not a reliable indicator of future investment performance and that no guarantee of performance, the return of capital or a particular rate of return is provided. It may not be reproduced, distributed or published, in whole or in part, without the prior written consent of Natixis Investment Managers Australia Pty Limited and IML.

Stay up to date

with Vaughan Nelson

Register to receive regular performance updates and regular insights from the Vaughan Nelson investment team, featured in the Natixis Investment Managers Expert Collective newsletter.

Vaughan Nelson Investment Management marketing in Australia is distributed by Natixis Investment Managers, a related entity. Your subscriber details are being collected on behalf of Vaughan Nelson Investment Management, and Investors Mutual Limited (the RE for Fund) by Natixis Investment Managers Australia. Please refer to our Privacy Policy. Natixis Investment Managers Australia Pty Limited (ABN 60 088 786 289) (AFSL No. 246830) is authorised to provide financial services to wholesale clients and to provide only general financial product advice to retail clients.